Being in debt is difficult, and if you’re in debt, you likely agree. Being in debt can be overwhelming and make you feel like you just can’t gain any traction. Are you ready to make some major changes to your finances and get out of debt once and for all?

There are many different debt repayment methods, but three of them stand out as the most effective ways to get out of debt.

The Best Debt Repayment Methods

Sure, there are more than just three debt repayment systems, but let’s be honest, you want to pay off debt FAST, right?

Constantly shuffling a few bucks on this credit card and a few bucks on that loan (on repeat) each month will just serve to keep you in this constant cycle with no end in sight.

And sure, if you stay consistent and steadfast, you will likely get out of debt at some point in your life, but newsflash: you weren’t born just to work and pay off debt!?

You, my friend, were born to thrive.

And you cannot thrive when you’re buried under a mountain of debt.

While it is important to remember that fixing your finances requires a lot of patience, time, and hard work, having a plan and taking action will help you get your debt paid off and take back control of your life.

Debt Snowball Method

This is the method we used to pay off $54,500 of debt in only 20 months, so it is near and dear to my heart.

It worked like a charm and, in my opinion, is the very best method if you are someone who quickly loses motivation, needs tangible reinforcement, or easily quits when you don’t see lightning-fast results.

Pro: This method will keep you motivated along your journey. It serves up quick wins and really helps you get some serious traction during the process.

Con: You may end up paying extra money in interest with this method since you’re paying off the smallest balance first (even if it has the smallest interest rate as well), and the debt with the highest interest rate might end up last on your debt priority list.

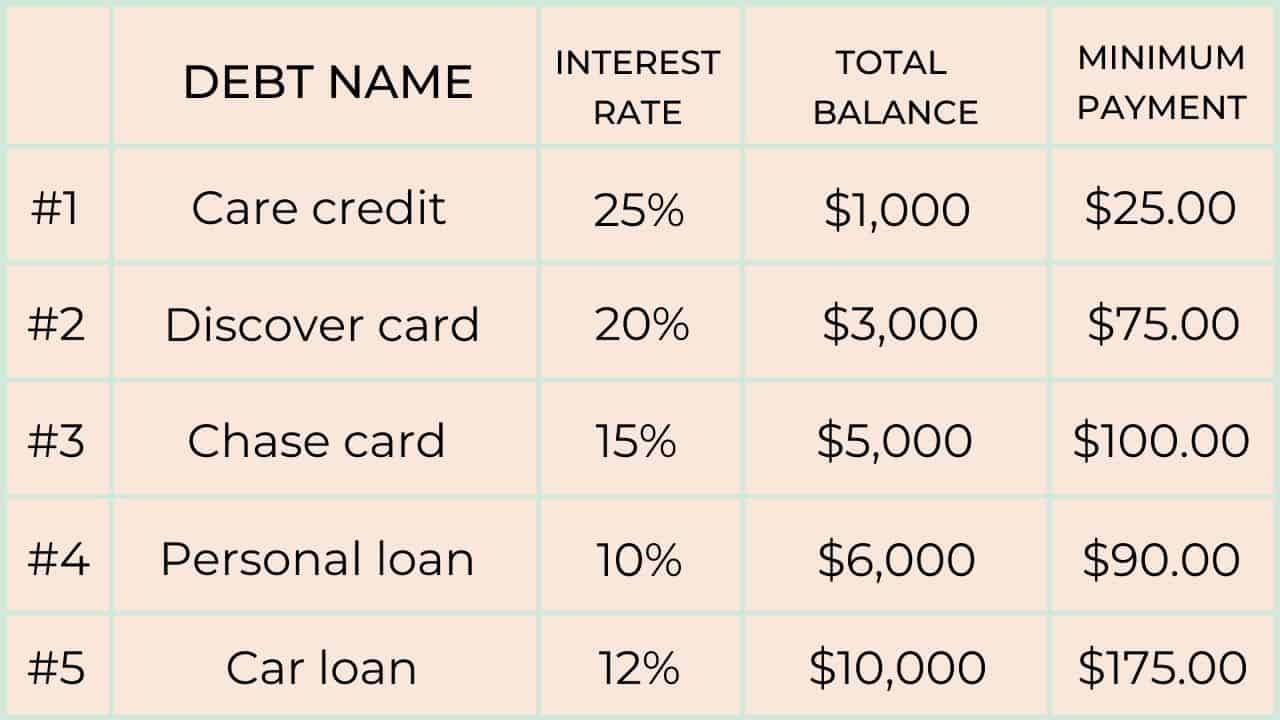

The Debt Snowball System works by taking all your debts and listing them in order of balance – least through greatest – with #1 being the lowest balance and working your way up.

If you’re a visual learner and need to SEE it to “get it,” have a look at the completely made-up, overly simplified charts to illustrate each method.

So if these are your debts below, this is how you would sort them to create a debt snowball as your debt repayment method.

With this method, you only focus on one debt at a time.

You will always make the minimum payment on all of your debts each month but will only focus on paying off one debt at a time.

Channeling all your focus solely on one debt allows you to clear that debt considerably quicker than if you were working to pay them all off at the same time.

After you pay the minimum on debts 2-5 (using the chart as an example), you take all the extra money in your budget, and add it to the minimum payment of debt 1, and put it all on debt 1.

Repeat this process each month, putting every dime you can find on debt 1 until it is paid in full. Congratulations, you just paid off your first debt.

This should feel amazing. This should give you confidence – both in yourself and your abilities and in this debt repayment system. You got fast results, and you’re motivated to keep pushing through.

You will now make the minimum payment on debts 3 – 4.

You will then take the minimum payment you were making on debt 1, plus all the extra in your budget, and add that to the minimum payment of debt 2 and put it all towards debt 2.

Repeat this process each month until debt 2 is paid off.

This example shows you how quickly you will start to gain momentum with the debt snowball method.

Debt Avalanche Method

The debt avalanche method is quite similar to the debt snowball method.

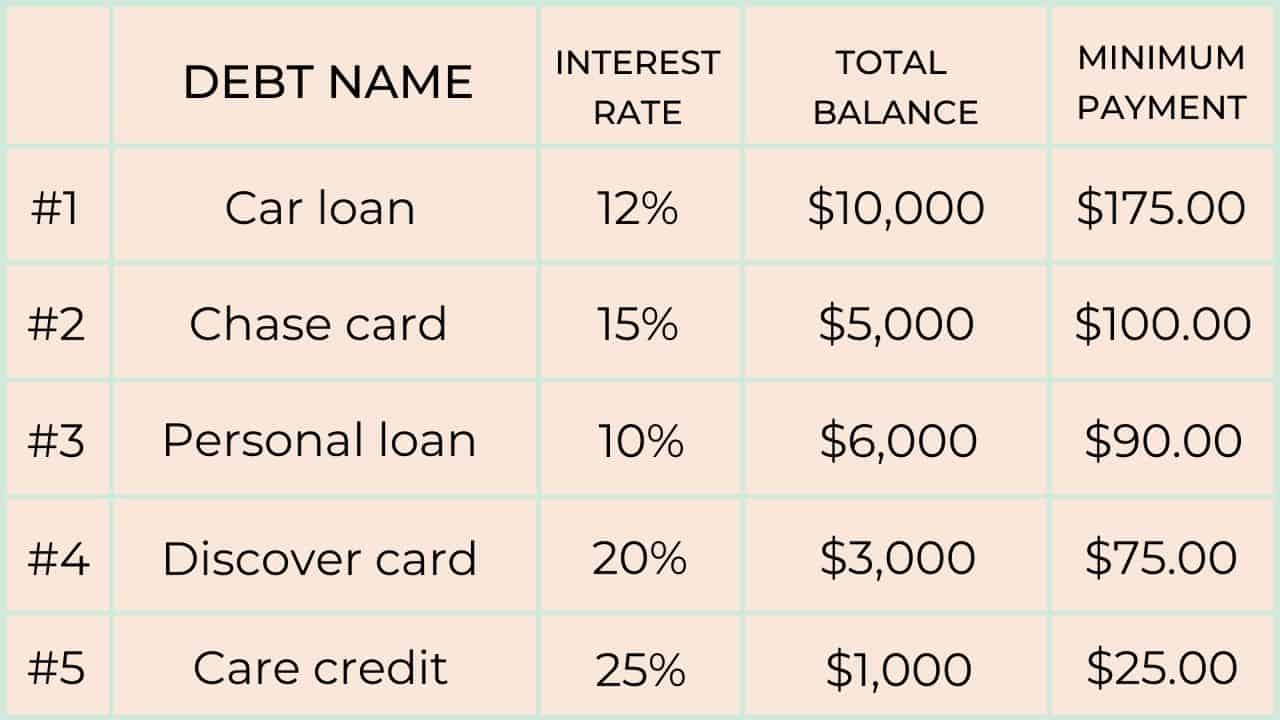

The major difference between the two is that with this system, you will sort and pay off your debts by order of interest rates.

Pro: You can save a few bucks in interest with this method. How much, however, completely depends on your balances, interest rates, and how fast you can clear all of your debt.

Con: It can take much longer to see substantial progress resulting in impatience and frustration.

Using the same numbers from our example above, here is the chart illustrating how to order your debts using the debt avalanche method.

Using this method, you will be clearing the debts first that are accruing interest at a higher rate. This method may be best for you if you don’t have as much money to put toward repaying debt.

The actual steps you take when repaying the debt are still essentially the same.

You will order your debts in the manner illustrated above, but you will pay them off using the same steps we outlined in the debt snowball method.

Clear debt 1 in its entirety while still making the minimum payments on all other debts.

Then focus on debt 2 and so on and so forth until you are free.

The debt avalanche method is a favorite for many, especially people who tend to be more focused on the details.

You may feel more accomplished if you are saving a bit extra in interest over the length of time it takes you to become debt-free. Though, in many cases using the debt avalanche system only results in minimal savings.

Yes, becoming debt-free as quickly as possible is preferred, but you must remain focused on the big picture. Remember, this is a marathon, not a sprint.

You may save a few hundred dollars in interest, but if that means you end up staying in debt a year longer, that doesn’t seem to make much sense in the long run.

Highest Payment Method

As you may have guessed, when using the highest payment method, you will pay off your debts by first paying off the balance with the highest monthly minimum payment.

The thought process here is that once this debt is paid off, it frees up a larger amount of money to put toward your debts each month.

Pro: This may be helpful if you are extremely strapped and have virtually no money to put toward debt each month.

Con: Depending on the size of the debt (as pictured below in our example chart), it could take a great amount of time to pay off your first debt, still leaving you with very little money that entire length of time.

As in the previous two methods, the steps will remain the same, but you will sort your debts as in the example in the chart above.

As you can see, paying off debt 1 first will give you considerably more money to work with each month than if you paid off debt 5 first, as you would if you were using the debt snowball or debt avalanche methods.

This isn’t often the preferred method, but it has its advantages in certain circumstances.

Plus…who doesn’t love options?

The bottom line is that you must determine the best method for you, which may not necessarily be the best method for someone else.

This is why it’s super important to sit down and have a money meeting with your partner or, if you’re single, an accountability partner who can help guide you in making the best financial decisions.

Here’s the Deal

Debt is a very personal subject, so it can be tough to reach out for help and advice. Take a look at these methods and determine which one is the best fit for your current financial situation.

Get on a budget right away, stop using credit cards, build a starter emergency fund, and switch to a cash payment system. Work hard and work fast.

Maybe even start a side hustle to help boost your income, so you have more money to pay off debt.

Lastly, take some time, put your numbers down on paper, and take a good look at how each method would play out for you.

Remember, you will save interest by using the debt avalanche, but the debt snowball is more rewarding and motivating, psychologically speaking.

The most important thing is that you get out of debt, regardless of the method.

Debt will continue to keep you from being free and fully enjoying your life but only for as long as you allow, so don’t wait any longer.