How many sinking funds categories do you currently save for? If you’ve been budgeting for a while, you probably know all about sinking funds and why they’re such an important component of a budget, but are your sinking funds actually protecting your budget when you need them to?

Do you have an adequate amount of sinking fund categories, or do you find yourself still coming up short on funds in your monthly budget?

💸 Take Back Control of Your Finances in 2025 💸

Get Instant Access to our free mini course

5 DAYS TO A BETTER BUDGET

If so, you may want to consider creating additional sinking funds to ensure you’re prepared for any unexpected expenses that may come knocking.

What is a Sinking Fund Budget?

Before we review each essential sinking fund category, let’s take a minute and talk about what the term sinking funds actually means, the purpose of a sinking fund, and how it fits into your budget.

Basically, a sinking fund is just a pool of money you save to cover an expense you expect will occur sometime in the near future.

Sometimes you know exactly when that expense will occur and what it will cost – as in your annual car insurance premiums, which are due at the same time every year.

Sometimes you have no idea what is coming – or how much money it will cost – but you have a reasonable expectation it will happen at some point, and you want to be prepared so you don’t have to accrue debt to cover these unplanned expenses.

Do You Need to Use Sinking Funds if You’re Already Budgeting?

Yes, in my opinion, they are a necessity and the best way to protect yourself from going into credit card debt or using your emergency fund unnecessarily.

Sinking funds don’t replace your budget – they support it.

Your budget, emergency funds, and sinking funds work together as a powerful financial team to ensure you’re prepared for anything that may come your way and allow you to avoid debt in any circumstance.

If you don’t have sinking funds and incur an expense you can’t afford to pay for with your regular income, one of three things will happen.

- You’ll take the money from your emergency fund. If this expense happens to be an actual emergency, then cool. No problem. But if it’s not, you risk getting into the habit of taking money out of your emergency fund every time you need a little extra, and before you know if you’ve depleted your emergency fund. *Skip to number 3*

- You will have to skip paying something else or cut/reduce another item in your budget to free up funds to cover this expense.

- You will have to use some form of debt to pay for the expense. Borrow from a friend or family member, charge it on a credit card, or take out a loan.

Is There Another Option?

Yup.

Creating and maintaining sinking funds in various categories gives you an extra source of money you can pull from to pay for specific expenses when they occur, allowing you to keep all of the other items in your budget untouched and intact!

What is the Difference Between an Emergency Fund and a Sinking Fund?

The terms “emergency fund” and “sinking fund” are often used interchangeably, but they are not the same thing.

Remember, sinking funds are used to prepare for upcoming expenses that will occur at some point in the future, like planning ahead for irregular bills or big purchases.

An emergency fund is one of the most important things you should have to protect your budget and your sinking funds from any number of unexpected expenses.

An emergency fund is used to prepare for expenses you don’t know will occur.

While you can be certain emergencies will happen – how, when, where, and how much they will cost are completely unknown.

And because it’s difficult to plan for the unknown, saving and maintaining an emergency fund will allow keep you from having to go into debt should you receive expensive medical bills stemming from a health scare or find yourself laid off from your job for a number of months.

Your emergency fund should be equal to anywhere from three to six months of expenses and has no purpose other than to hang out in a separate savings account in case of an emergency.

What Sinking Funds Should I Have?

That has to be a decision you and your spouse/partner make when looking at your specific budget and your specific financial needs.

If you’re someone who hates managing your finances and keeping track of multiple accounts, you may opt to consolidate and group a few different categories together.

It’s also important to note that just as your monthly budget is fluid, so should your sinking funds be.

If you find you no longer have the need for a specific category, rename it to something that is actually needed or gets rid of it altogether.

I’m not a big fan of overcomplicating things – it requires extra brainpower to maintain, often causes confusion, and eventually leads to failure.

Sinking funds support your budget and allows you to continue to budget consistently, so keeping your strategy simple and manageable will improve your ability to stick to your budget!

Sinking Funds Categories

Because we all have different financial needs and different budgets, we likely have different amounts and types of sinking funds as well.

Many people take a “less is more” approach when it comes to sinking funds in an effort to keep things more streamlined and avoid confusion.

But if you are living on a tight budget, you may find it beneficial to create additional sinking funds.

Having more sinking funds can minimize borrowing from other sinking funds (or your emergency fund) to cover an unexpected expense.

Let’s discuss seven essential sinking funds categories that may be a good fit for you and your budget.

Some of these may not apply to you, and that’s ok.

Feel free to replace them with a different category or scratch them off your list altogether.

I have included them because while they might not be crucial to everyone if they are applicable to you, it’s likely they represent an essential part of your life and your budget and should be included.

Christmas Fund

For most of us who celebrate Christmas or even Channukah, yes, it’s a known expense, but it often requires a large chunk of change.

There is nothing worse than working hard on your finances all year long only to have the holiday season roll around and have to pay for all your Christmas gifts with a credit card because you have no extra money.

You didn’t prepare for it…as if it doesn’t come on the exact same day every. single. year.

The good thing is, you’re not alone…last year, 36% of Americans reported taking on holiday debt.

Determine the total amount of money you’ll need to pay for the holidays and stash some money in your Christmas sinking fund throughout the year.

By the time you’re ready to begin your holiday shopping, you’ll have the money you need to cover the big bill!

Being intentional and saving money for the specific purpose of paying for all of the holiday madness celebrations is a great way to guarantee yourself peace of mind at the end of the year instead of worrying about the credit card bill that’ll be showing up in January.

Additional items that can be covered with your Christmas sinking fund:

- expenses for other holidays (Thanksgiving, New Year)

- meals

- parties

- decor

- holiday cards

- and more…

Home Fund

This category is one of the most important.

If you’re a homeowner (or a renter who is responsible for home maintenance), you know how quickly you can burn through your savings when big expenses like home repairs need to be done.

Building up a nice chunk of change in a home sinking fund account will be a lifesaver the next time your hot water heater floods your basement or your central air goes out…on the hottest day of the year (because that’s the way it always works, right?).

Another good idea would be to create separate savings where you can save a small amount of money each month to prepare for large expenses down the road, such as a new roof.

It’s possible your roof may be in decent condition, but you know within the next 10 years, or so you will want to replace it.

Instead of allowing the need for a new roof to surprise you one day and eat into your emergency savings, preparing in this long-term manner will allow you to save for future expenses way in advance.

This strategic way of saving will allow you to put away a little bit of money each month without much impact on your financial health.

Additional items that can be covered with your home sinking fund:

- school and/or property taxes

- insurance

- HOA fees

- upgrades

- and more…

Kids Fund

If you’re a parent, you know how expensive kids are…they’re lucky we love them so much.

Keeping a specific sinking fund just for your child-related expenses won’t make them any less expensive, but it will help you be more prepared when they’re nickel and dime-ing you to death.

From book fairs to field trip slips brought home the night before, this category has come in handy more than you know.

Additional items that can be covered with your kids sinking fund:

- sports fees + equipment

- school supplies

- allowances or commissions

- birthday gifts for parties they attend

- clothing

- and more…

Medical Fund

If there’s one thing that can quickly derail your financial goals, it’s medical expenses.

A medical sinking fund is your weapon against random illnesses…that inevitably spread to the whole family.

It will also have your back when you get prescribed an expensive (yet, necessary) medication and are charged costly co-pays.

This is a good category to prioritize, especially if your medical insurance is less than stellar.

Additional items that can be covered with your medical sinking fund:

- co-pays

- prescriptions

- hospital bills

- doctor fees

- vision costs

- dental costs

- and more…

Note: If you are on a high-deductible insurance plan, be sure to research HSAs (Health Savings Account). HSAs function partly as separate savings accounts and partly as investment accounts.

Pets Fund

We sure do love our furry friends, but they are notorious for costing a pretty penny.

When our pup suffered a serious bout of pancreatitis, our vet bill cost more than our mortgage payment!

Yet, of course, we want to do everything we can to keep them healthy, but sometimes our budgets just don’t have enough margin to come up with a few hundred – or thousand – dollars when Fido decides he wants to chow down on a plant that doesn’t sit well with him.

This is exactly why if you’re a pet owner of any kind, you need to have a pet sinking fund.

I promise you the day will come when you are grateful you had the foresight to set up this fund – that way, you’ll never have to choose between paying the pet expense to save your kitten’s life or making your rent payment!

Additional items that can be covered with your pet sinking fund:

- pet insurance

- food

- toys

- gear

- pet sitter

- and more…

Vacation Fund

Ahh, remember the pre-pandemic days when we could travel and book a vacation in advance – and actually get to enjoy it instead of having to cancel?

Yeah, me too…I’m confident we’ll be back in that place someday (hopefully sooner than later), so I’m still contributing to my vacation sinking fund – and I think you should too!

Not all vacations have to wipe out your entire savings account, but why use your regular savings account to fuel your wanderlust?

Just start a vacation sinking fund, and by the time you book an epic family vacation, you may even have enough money in there to fund the entire trip or at least some extra spending money to take along for excursions and other fun things to do!

Additional items that can be covered with your vacation sinking fund:

- road-trip tolls

- car rental

- plane tickets

- pet/house sitter

- Uber fees

- and more…

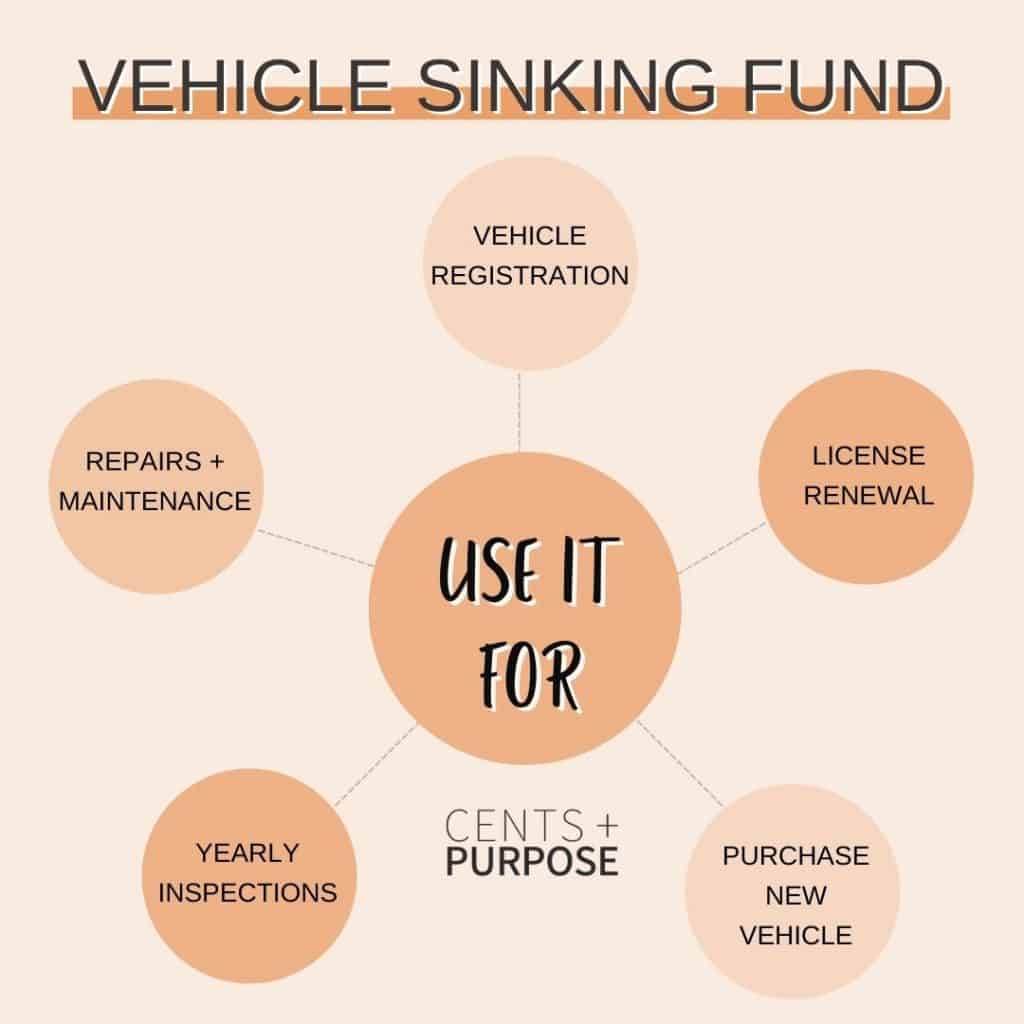

Vehicles Fund

Last but definitely not least is a vehicle sinking fund…this one is also very important.

Listen, you may be driving Ole’ Faithful around town, but it’s inevitable that at some point, you will need to fund some car repairs or, at the very least, regular maintenance, such as new tires and oil changes to keep your car running as efficiently as possible.

Unless you’re an experienced mechanic, chances are you’ll have to foot a decent-sized bill.

Imagine how good it would feel to have the money you need sitting around in a sinking fund, just waiting for the day you need to use it!

Additional items that can be covered with your vehicle sinking fund:

- car maintenance

- gas

- inspections

- license renewal

- and more…

How Do You Organize Your Sinking Funds?

Simple. However you want.

Personally, I group a bunch of my sinking funds together with other spending categories and categorize them all into different online bank accounts.

I also keep a written log (because I’m a super nerd) in my budget binder so I can quickly check any of the balances at any given time without having to log in to my bank account.

You can keep a notebook and track one sinking fund per page, record them on a sheet of plain paper, or use your favorite budgeting app to organize your sinking funds.

If you’re using sinking funds to save for long-term goals such as a new car or a down payment on a home, you may want to consider keeping them in their own separate sinking funds instead of mixing them with the vehicle and/or home maintenance funds for simplicity.

Find a way that feels easy and convenient to you, or you won’t do it…

Where Should I Keep My Sinking Funds?

Your sinking funds can be kept anywhere that is separate from your main checking account.

I recommend high-yield savings or checking accounts (depending on how often you may need to use the fund) or even cash envelopes if you prefer your sinking funds more liquid.

Sinking Funds FAQ’s

Here are a few questions I see often regarding sinking funds you may find helpful:

How Much Should I Put in a Sinking Fund?

There is no set amount of money that is required to be saved in a sinking fund.

A good rule of thumb is to determine the total amount you need and divide it by the number of months you have to save.

This will give you the amount of money you should save in that sinking fund each month to reach your goal.

What are Good Sinking Fund Categories?

While all of the sinking funds examples listed above are important, many of them may not apply to you.

In addition, there may be many other sinking funds categories that do apply to you and were not included in this list.

Any expenses that could be considered short-term savings goals, irregular expenses, or large purchases could probably be a good sinking fund category.

How Many Sinking Funds are too Many?

There is no specific number of sinking funds you should have and no amount of different sinking funds that are too many.

Personal finance is personal – that means that the number of sinking funds that work best for you and your budget will likely be different than the amount that is right for the next person.

Rather than focusing on a specific number of funds you should have, a better way to determine your needs would be to review all the expenses you pay throughout the year.

Determine which are regular monthly expenses – these known expenses are usually listed as a line item in your monthly or pay period budget and, therefore, would not require a sinking fund.

Items remaining on your list are likely non-monthly expenses or periodic expenses. This means they are paid on a quarterly, bi-yearly, or annual basis.

While these would not necessarily be considered a “last minute” expense, they can often feel like it when the bill arrives or your credit card is charged for a bill you had completely forgotten about.

These types of expenses would be good candidates for sinking funds and could be something as simple as your Amazon Prime renewal or as important as your accountant’s fee for preparing your income taxes.

That covers the seven essential sinking funds categories you need to budget better, but remember, this is far from an exhaustive list.

You can create a sinking fund for literally anything your heart desires, so don’t limit yourself to only the funds mentioned in this blog post – do what feels best for you and your personal financial situation.

What do you think of this list? If you already use sinking funds as a financial tool, which categories do you use already?