Living on a budget is crucial when working towards reaching your financial goals but creating and sticking to a personal budget is only half the battle. The act of balancing a budget at the end of each budget period is an essential part of the budgeting process that many people skip.

While balancing your budget is a simple task, it’s not always easy and can take some time, especially if not done consistently.

💸 Take Back Control of Your Finances in 2025 💸

Get Instant Access to our free mini course

5 DAYS TO A BETTER BUDGET

Balanced, Closed Out, Reconciled

Before we get started with the step-by-step tutorial on balancing your budget, I want to clarify that the idea of “balancing a budget” is often also referred to as “reconciling a budget” or “closing out a budget.”

And while different people may balance their budgets using a different process or use different terminology, it all means the same thing.

Balancing, reconciling, or closing out your budget is simply the process of comparing your initial spending plan (that’s just a fancy word for a budget) with how your budget period actually played out – because if you’ve ever tried to budget before, you know the two rarely have the same result.

Why You Need To Balance Your Budget

If you’re new to budgeting, it’s very possible you never even knew this step existed – I didn’t for the first few months I was budgeting.

Any time I heard the phrase “balancing a budget” it usually had some type of official or governmental context…I never knew balancing a personal budget was a thing.

And once I did, I didn’t quite grasp the concept, so I decided I didn’t want to bother with balancing my budget.

However, once I finally began to include this step in my budgeting process, I found it extremely helpful, and these days I never begin a new budget period without closing out the prior.

Prioritizing the task of balancing your budget has a few advantages:

- It will give you useful information about your spending habits

- It will give you a clean slate to begin your next budget period

- It ensures your budget and your bank account are matching and in-sync

- It will give you a better understanding of your budget and your finances as a whole

- It will allow you to pursue your financial goals with less stress and more confidence

What is a Balanced Budget?

Technically, this could depend on what type of budget you use, but essentially (or for the purposes of this article, at least), what makes a budget balanced is:

- It matches your bank account (in both transactions and balance)

- It includes accurate figures for income, expenses, spending, and saving

- It ideally balances to zero when total expenses are subtracted from total income

Whether you budget on a monthly, bi-weekly, or by paycheck basis, making sure your budget meets the above criteria will ensure you are beginning a new budget period with a clean slate – meaning there are no transactions outstanding or unaccounted for that could throw a wrench in your next budget period.

Should You Balance Your Budget Each Month?

Not necessarily. It’s important to note that your budget period and your reconciliation period should be the same.

If you budget each month at a time, then you need to be balancing your budget at the same frequency.

If you budget each paycheck by itself, then you also need to balance your budget at the end of each pay period.

If you haven’t been successful with getting your budget to balance in the past, it is likely because you haven’t been synchronizing your budgeting and your reconciliation time periods.

Which is the Best Way To Balance Your Budget?

Whether you’re using a budget app, a budget binder, or a budget spreadsheet, you can balance your budget.

Each budget app or other software program will be unique in its features but will likely include some type of option to reconcile your accounts.

Otherwise, regardless of whether you use a spreadsheet or pen and paper, the balancing process will be very similar.

Depending on the type of budget spreadsheet you use, there may or may not be available space and formulas already included to use when balancing your budget.

If that’s not the case with your spreadsheet, you may choose to format the spreadsheet on your own (I don’t recommend this option unless you’re well-versed in using spreadsheets) or simply “do the math” on a spare sheet of paper using the information from your spreadsheet.

Balancing Your Budget in 3 Simple Steps

If you’re already feeling overwhelmed by the thought of balancing your budget because you’re not yet successful with creating a budget, you’ll want to start by signing up for my free budget course.

You’ll get five lessons and a free workbook with helpful budgeting worksheets and trackers (the steps and images included in this post were created using the budget worksheet from the free workbook).

Note: It’s helpful to wait to complete the process of closing out your budget as close to the beginning of your new budget period as possible. This will decrease the amount of time when new transactions could occur in the budget period you’re closing out and offer you the most accurate numbers and data in your bank account.

To get started, grab your budget worksheet (or spreadsheet), and be sure you can access your bank account and credit card(s) if you use one.

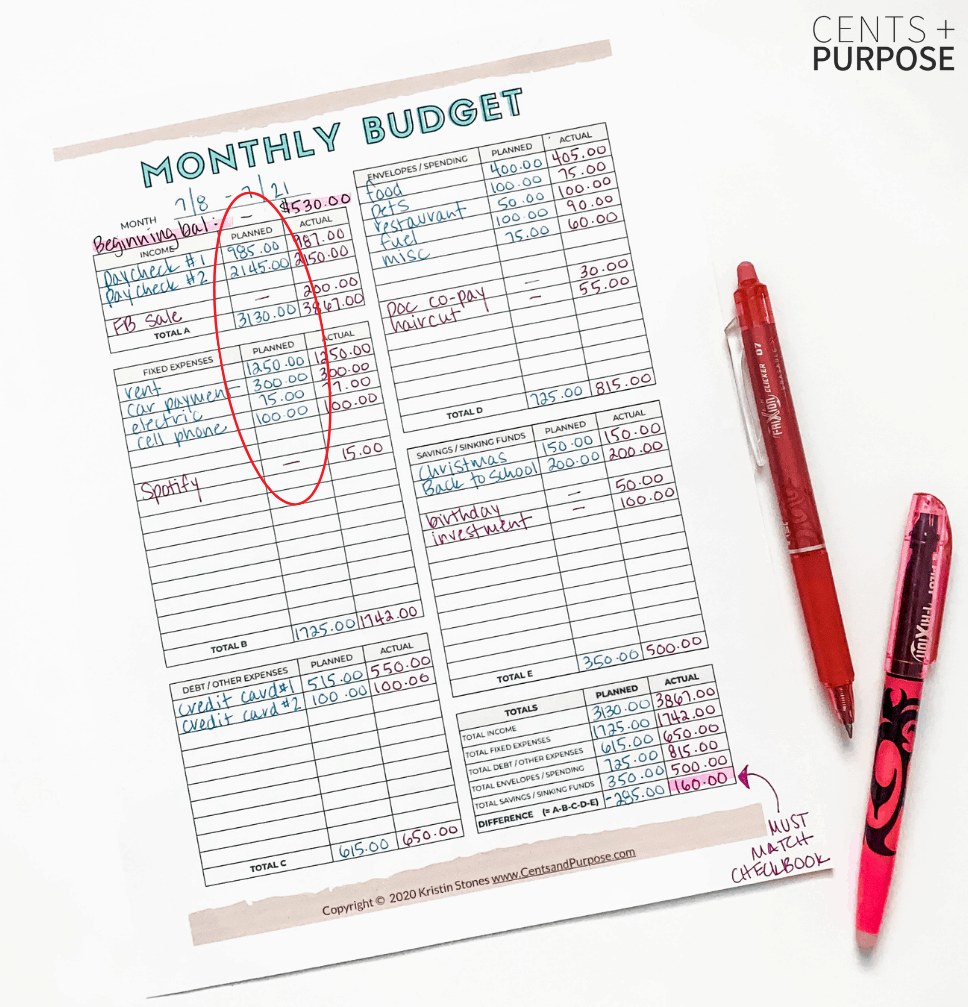

1. Update Your Income

First things first.

You can’t pay any bills without any money, so we’ll begin with the income section.

If you run your finances as I do, you probably have one main account that acts as your “operating account” or “main hub” as I call it.

This is likely the account your paycheck(s) are deposited into and the account from which all (or most) payments and any transfers are made.

This is the account you will need to reconcile your budget against to make sure it’s balanced.

If you reconcile your checking account against your bank statement each month, this process will feel familiar to you.

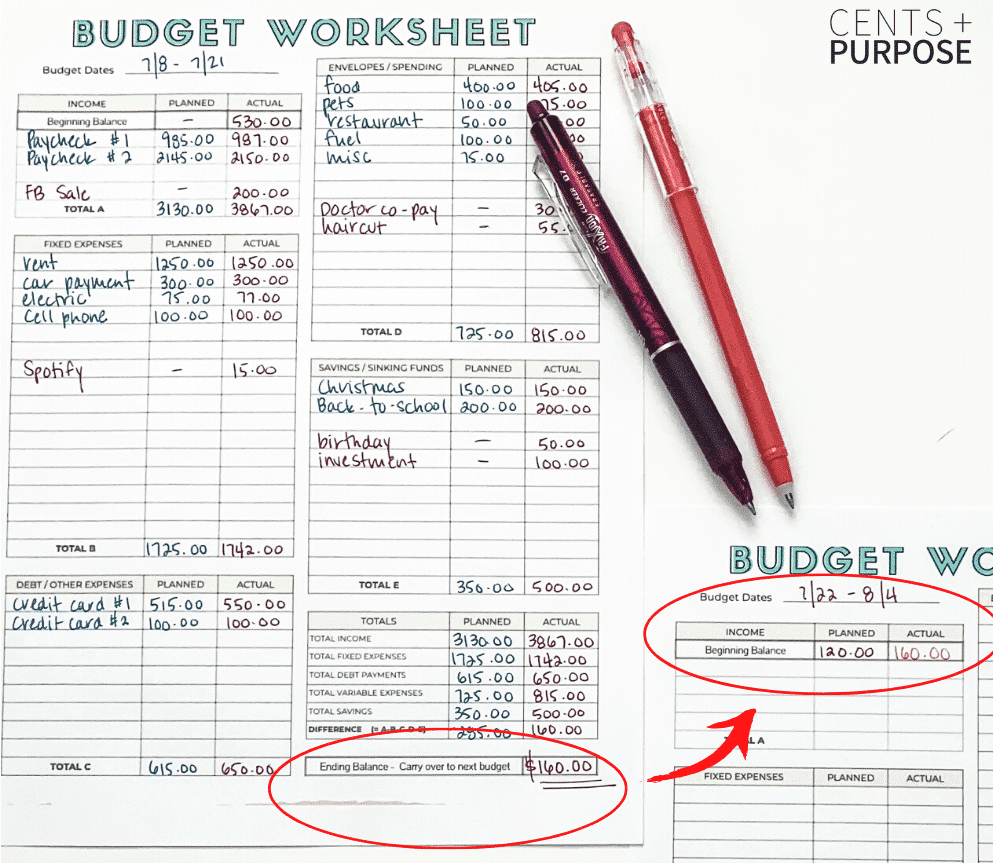

Complete the “Actual” Column

Remember, the point of a budget is to create a plan for your money before the money actually arrives in your bank account.

When creating your original budget – or spending plan – you’ll be filling in your income and expenses plus any debt payments you plan to make and any money you plan to save.

Since your budget or spending plan is simply an estimate of what you plan to do with the money you will be receiving, therefore, when creating your budget, you’ll be entering the amounts into the “planned” column.

When reconciling transactions that actually occurred throughout the budget period we will be focusing on the “actual” column and working our way through the worksheet entering the amounts that were actually received, paid, spent, and saved.

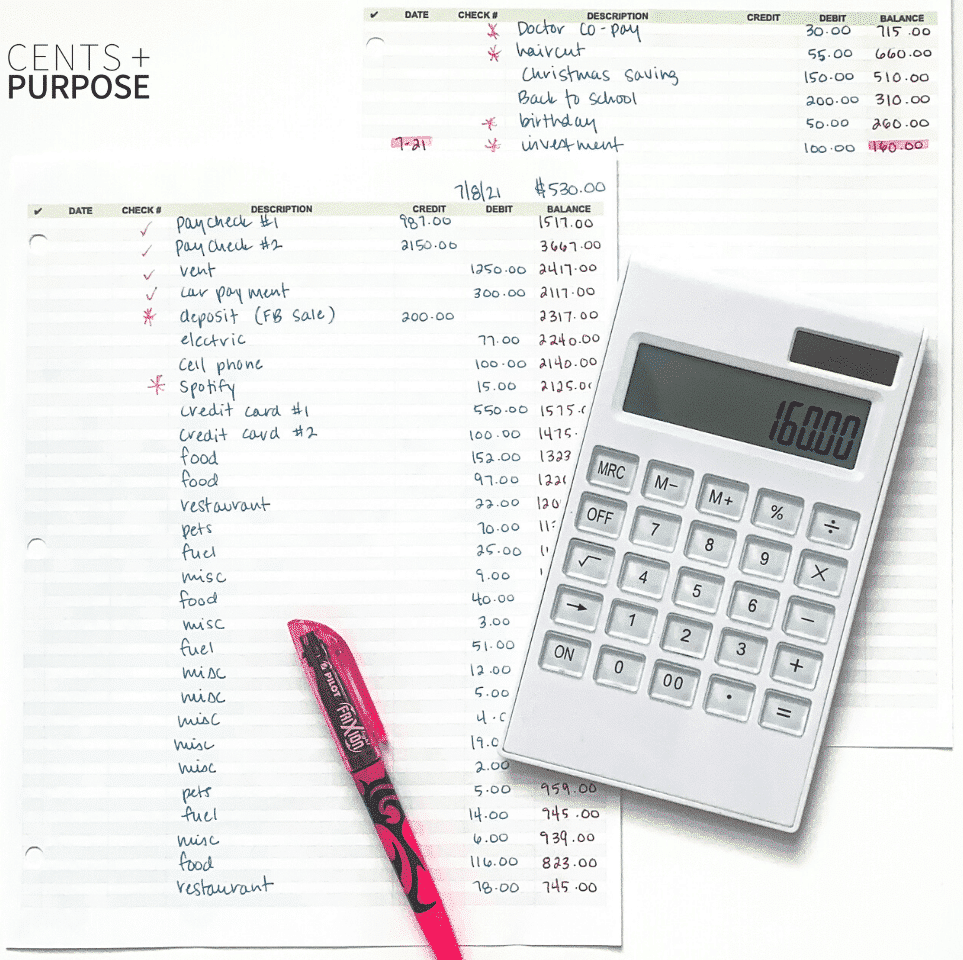

Next, enter all actual income received in the budget period in the “actual” column.

Personally, I like to use a colored pen when I create my budget initially and switch to a different color when I’m reconciling my budget because it allows me to visually separate things (I don’t know why…my brain works funny).

Fill in the “actual” column with the exact numbers of your income.

If you’re salaried, your “planned” and “actual” columns will probably look the same for your income, but if you budget on an irregular income, they may look very different.

It’s important to include any deposits into your bank account as “income” when reconciling your budget.

This may feel strange if the money deposited into your account is not necessarily earned income, but for the sake of simplicity when it comes to budgeting, we categorize all transactions as either income or expenses.

I know this is a sticking point for many, so I’ll give you an example:

If you return an item you purchased to the store and the store processes a credit to your debit card for the return (and this transaction occurs during the budget period you’re reconciling), you’ll want to enter that credit into the “income” section.

The money was received back into your bank account, so it must also be added back into your budget to keep it balanced.

Think of one of those old-time scales where you can place items on a dish on either side, and they will move up or down as you add or remove items.

If you visualize one side of that scale as your budget and the other as your bank account, it makes sense that when you’re adding money back into one side (as in the store credit example above), it will be out of balance until you also add that same amount to the other side of the scale.

If this concept still feels confusing to you try looking at “income” as any money coming into your account and all of the other sections such as expenses, debt, and savings as “outgoing” money since it is money going out of your account.

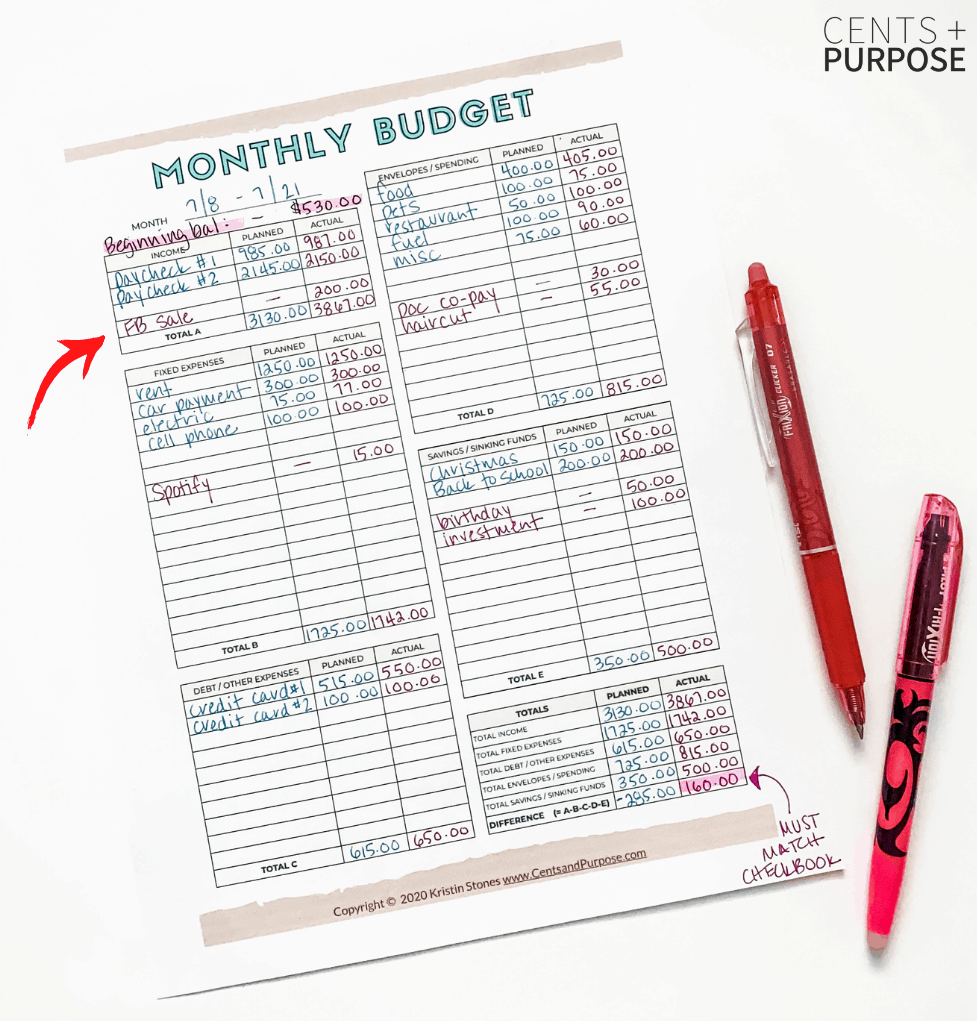

Additional Transactions

After you update the actual numbers of your paycheck(s) you’ll want to review your bank account and update your budget worksheet with any other money that was received during the budget period.

As noted above, these transactions would also be added to the “income” section of your budget worksheet.

Again, I typically like to enter any additional income/expenses (above and beyond those that appeared on my original budget) in a different color – if you’re also a visual learner this may be helpful to you too.

For this step, I like to open my checkbook and look to make sure I’ve added all additional deposits to my budget worksheet.

Note: You can also choose to enter a 0, a -, or leave the “estimated” column empty for any additional transactions you’re adding to your budget worksheet (or spreadsheet).

2. Update Your Expenses

Once you’ve completed the “income” section, you’ll use the same process to update all your expense sections.

Again, remember, when budgeting, we are focusing on two types of transactions: income and expenses.

Simply put, if the money comes into the account, it’s income, and if it goes out of the account, it’s an expense.

At the risk of sounding redundant, I want to reiterate this concept because people are often confused when I refer to debt payments and especially savings as an “expense.”

Since you’re taking the money you’re saving out of your account and moving it into a savings account or into an investment, it’s considered an expense on your budget worksheet.

Continue through each section of your budget worksheet using this same method of cross-checking your budget with your bank account and updating any expenses, debt payments, or saving amounts in the “actual” column.

Note: If you’re newer to budgeting, you may find it helpful to save the “spending” section until you’ve finished all of the other sections.

Be sure you’re checking for any additional transactions which occurred that weren’t in your original spending plan and add them to your worksheet.

You want all money coming out of your bank account reflected in one of the expense sections of your budget worksheet.

If there are any transactions you had initially entered in your budget but ended up skipping or pushing them back to a later budget period, now would be a good time to make a note or add it to the next budget worksheet, so it’s not forgotten.

Note: It’s also important to remember to enter a 0 in the “actual” column for these types of expenses, or your budget won’t balance.

Updating the “Spending” Section

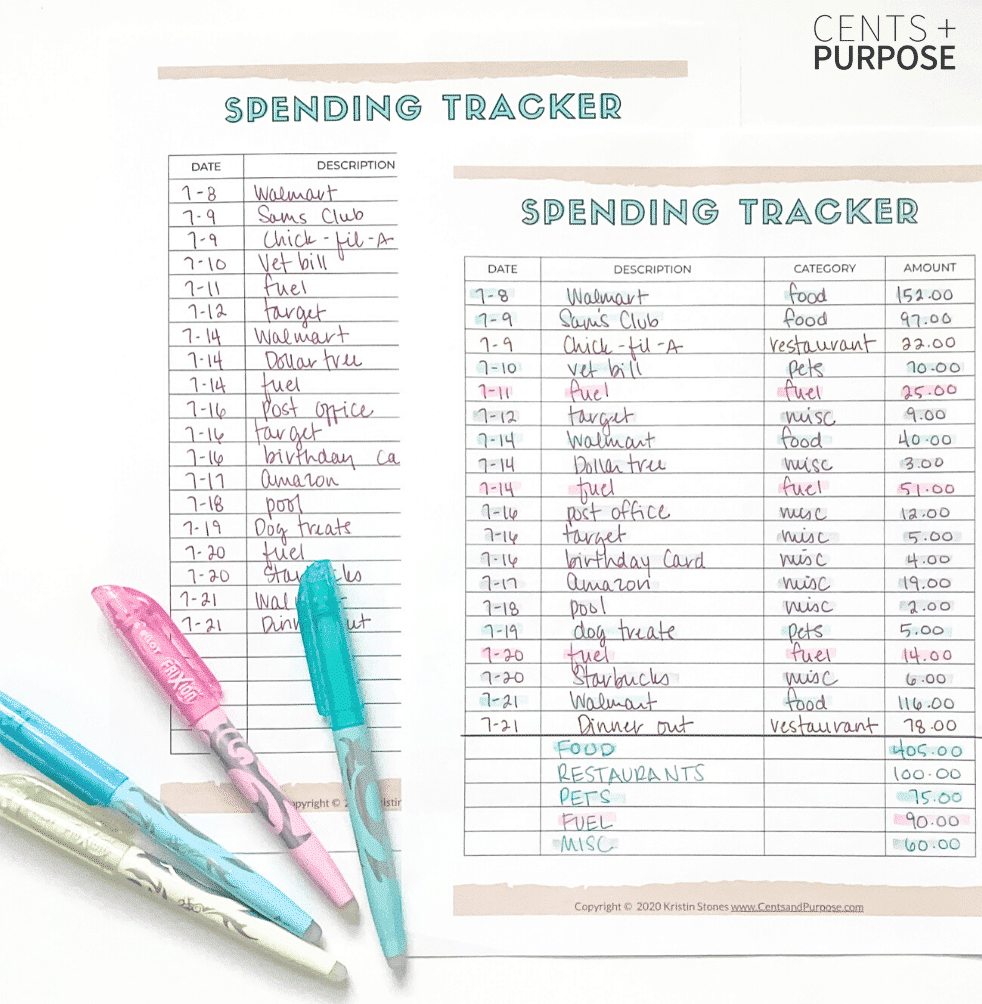

If you’ve been following my method of budgeting and managing your money then you’ve also been tracking your spending and probably have a good amount of spending data you need to reconcile.

Grab your spending tracker (whether it be my spending tracker, an app, or a spreadsheet) and find the total for all of your spending categories.

If using an app or a spreadsheet, you can grab the total amount for each category and enter it in the corresponding “actual” column.

If using a paper spending tracker, grab some colored pens or highlighters and circle or highlight each expense in a different color according to its category.

Ex: Groceries/Green, Gas/Pink, Restaurants/Yellow, etc.

Grab your calculator and add up all the transactions in each spending category to get the total spend for each of your spending categories, then enter each total in the “actual” column for that category.

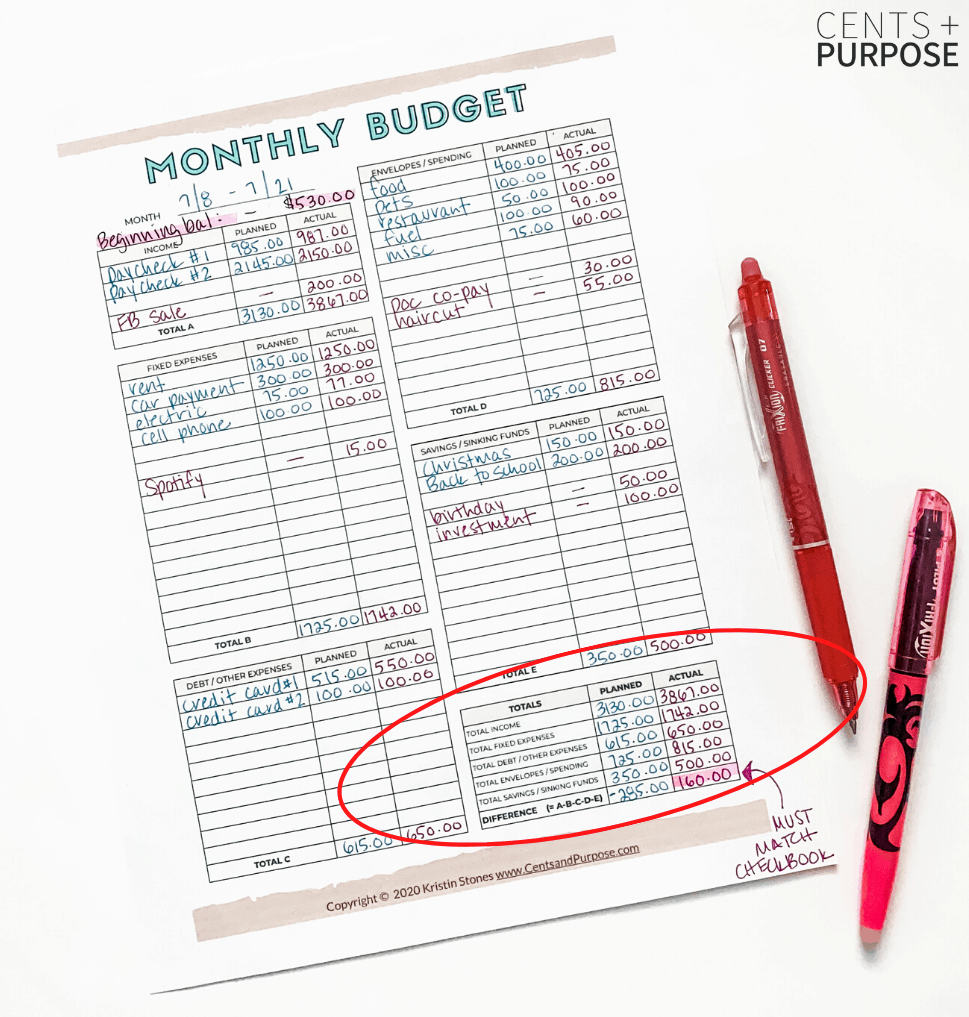

3. Compare the Numbers

At this point, you should have all additional transactions entered into your budget worksheet, plus all the “actual” fields should also be completed.

The final step is to do the math on your budget worksheet to find your budget total.

That number should match the current balance in your checking account.

If it does, you have successfully balanced your budget, but if it does not match, you’ll have to do a bit of troubleshooting.

Troubleshooting Budget Problems

If you can’t get your budget to balance, never fear…it’s likely you wrote down a number incorrectly, made a mistake with your math, or missed an outstanding transaction somewhere.

For example, if you wrote a check and have it noted in your budget and it hasn’t cleared your bank account yet, your bank account balance will show as higher than your budget balance.

Take a few minutes to review your bank account and account for any transactions that may still be pending.

If you don’t find this to be an issue, move on and double-check your math.

If you’re a math genius and your calculations were spot on, you likely missed a transaction somewhere along the way.

Go back through every transaction that appears in your bank account for the entire budget period, and be sure you have updated your budget worksheet (or spreadsheet) to include each one.

Note: If you have a credit card you need to pay off during this budget period, be sure you’re including that payment amount as an expense.

A Good Budgeting Habit

The last thing I want to mention is once you finish balancing your budget, you’ll want to get in the habit of taking the Ending Balance and copying it over to the Beginning Balance line in the income section of your budget worksheet for the next budget period.

Personally, I like to estimate what I think my ending balance will come in at when I sit down to create my new budget, as I usually prepare my new budget a few days before the new budget period begins.

I will enter my estimate in the “planned” line, and when I close out my current budget period, I will then enter the Ending Balance amount in the “actual” column in the Beginning Balance line on the new budget worksheet.

If you’re unsure of why we would enter the Ending Balance as “income” in the next budget, remember what we touched on earlier – when budgeting, we are classifying everything as either income or an expense.

Since the balance is money we already have in our account and it is money we are not transferring out of our account as savings or an investment, we must list it as income.

Theoretically, this is money (which was not used) we are carrying over from the last budget period to the new budget period, so we are able to use it if needed.

This step is not required to balance your budget; however, it’s a good habit to get into.

It can serve as a reminder that you did, in fact, balance the previous budget period and an indicator that no additional transactions occurred between the time you closed out one budget and began a new one.

Moving Forward

You did it; you’ve balanced your budget!

Now you’re able to confidently put any extra money you have towards debt, savings, or any other financial goals you’re pursuing without worrying that you’re using the money you needed to allocate elsewhere.

This process also offers you a ton of valuable data about your actual spending habits (not just what you “plan” to spend).

You can use this data to adjust your budget, set future goals, and understand strengths and weaknesses, financially speaking, all actions that will serve you well throughout your financial journey.

If you found this guide to balancing your budget a helpful resource, I’d love it if you shared it on Pinterest or Facebook or with someone in your life who could benefit from this budgeting skill.