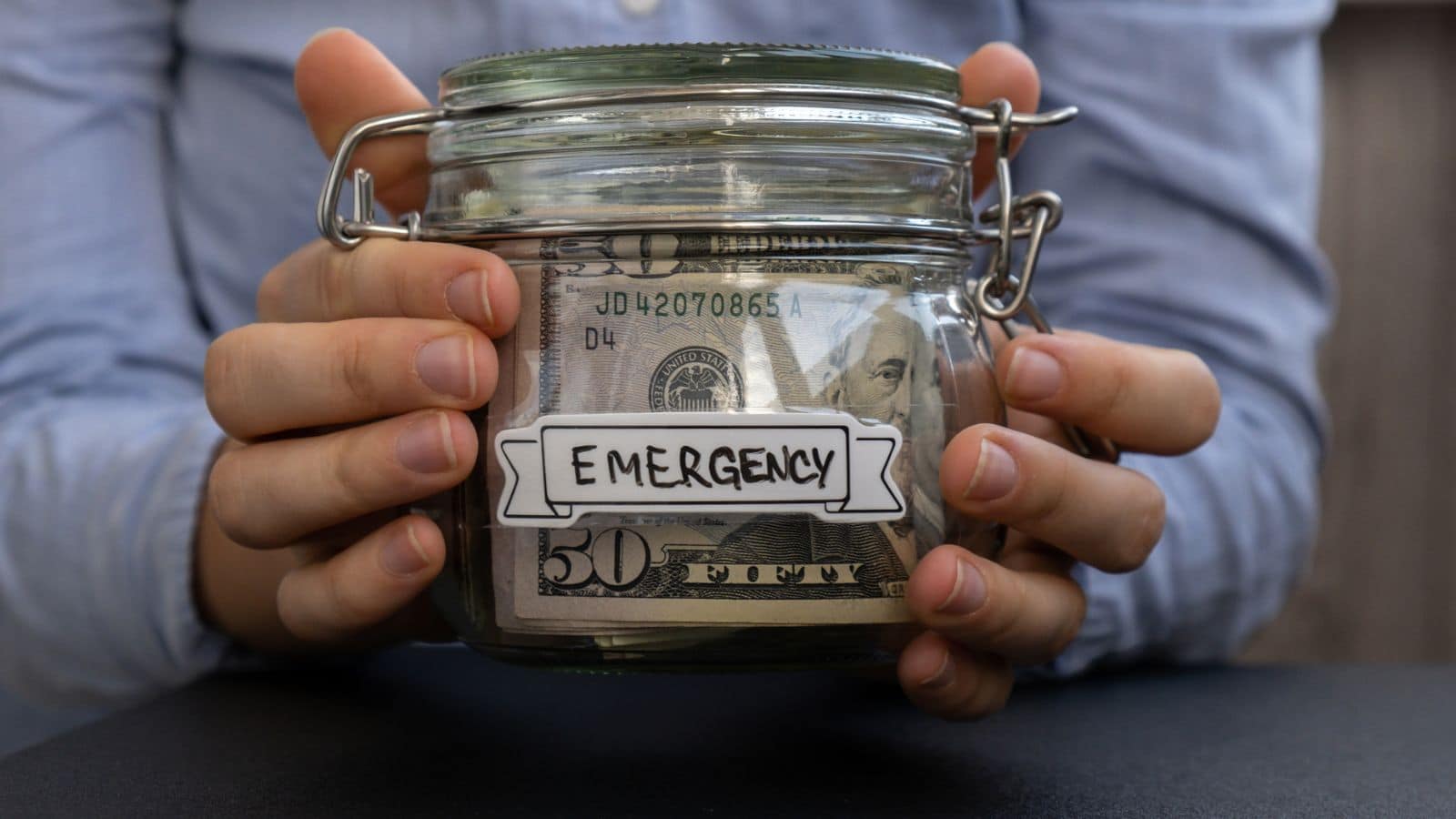

Your emergency fund is meant for real surprises, not every expense that pops up. It’s easy to blur the lines and use that money for things like trips, routine car maintenance, or yearly bills. But when you dip into your safety net for these planned costs, you risk coming up short when something truly unexpected hits. If you want your fund to actually help in a crisis, here are seven things it shouldn’t cover.

Non-Emergency Purchases

Your emergency fund is for true emergencies, like a car repair or a medical bill. It’s not for things like replacing your couch, getting a new phone, or going on a vacation. These are regular expenses that should be planned for in your regular budget, not pulled from your emergency savings. Keeping those purchases separate will help ensure your emergency fund stays intact for actual emergencies.

💸 Take Back Control of Your Finances in 2025 💸

Get Instant Access to our free mini course

5 DAYS TO A BETTER BUDGET

Subscription Services

Even if you’re just paying for one or two subscriptions like streaming services, these aren’t emergencies. You should be able to cancel or pause these services without too much hassle if needed. Subscriptions are ongoing, predictable costs, and they don’t belong in your emergency fund, which should be reserved for unexpected events. Make sure these types of expenses are part of your regular budget instead.

Luxury Expenses

It’s easy to get into the habit of thinking you can dip into your emergency fund for a treat or luxury expense, but that’s not what it’s for. Want to buy a new handbag, get a massage, or splurge on a fancy dinner? That’s not an emergency. Your emergency fund is there for things you absolutely can’t avoid, like medical bills or car repairs, not things you want to have but can live without.

Down Payments for Large Purchases

If you’re saving up for a big purchase, like a car or home, that’s great—but your emergency fund shouldn’t be the place to stash those savings. Your emergency fund is for urgent, unforeseen expenses, not planned big-ticket purchases. Set up a separate savings account for things like a down payment on a house or car so your emergency fund stays focused on its primary purpose: giving you a cushion when life throws a curveball.

Money for Special Occasions

Planning for holidays, birthdays, or other special events is important, but it shouldn’t be tied to your emergency fund. These are predictable events that you can budget for, so there’s no need to drain your emergency savings for these expenses. Instead, set aside a small monthly amount in your regular budget for gifts, parties, or special activities so they don’t interfere with your emergency fund.

Debt Payments

While it’s important to pay down debt, your emergency fund shouldn’t be the place you pull from to make regular debt payments. If you’re using your emergency savings to pay down credit card debt or loans, you’re not leaving yourself with a financial cushion when an actual emergency hits. Prioritize paying off debt through your regular budget and avoid relying on your emergency fund to cover monthly payments.

Investment Contributions

It’s tempting to use your emergency fund to start investing or add to your existing investments, but that’s not the right place for that money. Investments come with risks, and they should not be considered part of your safety net. Your emergency fund should be liquid, safe, and easily accessible—exactly what you need in a crisis. Investments can be made in a separate account when your emergency fund is fully built and you’re in a stable financial position.

Large Expenses That Aren’t Urgent

Sometimes, there are expenses that come up that feel urgent but aren’t actually emergencies. For example, if you decide you want a new car but your old one still works, it’s not an emergency. It might be tempting to dip into your emergency savings, but this should be a planned expense, not something that threatens your financial stability. Avoid using your emergency fund for items you can plan and save for in advance.

Keep Your Emergency Fund Focused

Your emergency fund is a critical tool for staying financially secure in times of need. But it’s easy to let the lines blur and start dipping into it for things that aren’t true emergencies. Keeping your emergency fund dedicated to only the most urgent, unexpected situations will ensure you have the money you need when life throws a curveball. Focus on building a solid foundation, and your financial future will be that much stronger.

9 Ways an Emergency Fund Can Protect Your Finances

Having an emergency fund is a necessary foundation of stability, yet many people overlook its importance until they face a crisis. It can be difficult to prioritize saving when life happens, but if having an emergency fund is so crucial, then why do so few people have one? Often, the same reasons people don’t have an emergency fund are the exact reasons they need one…here are nine examples. 9 Ways an Emergency Fund Can Protect Your Finances